Scam Attempts Have Become a Daily Reality for Most Americans

Fraudulent calls, texts, emails, and social media messages have stopped being occasional nuisances and become a near-constant feature of American life. A new AP-NORC poll finds that most Americans are inundated with scam attempts on a daily basis, a volume of contact that has shifted the experience of being targeted from something unusual to something almost expected. The sheer frequency means that even people who consider themselves careful and skeptical are operating in an environment designed to wear down their defenses.

About 3 in 10 Americans have personally lost money or personal information to scams.

That figure – roughly 30 percent of the country – translates to tens of millions of people who have already crossed the line from being targeted to being harmed. Personal information losses carry consequences that can stretch for years: compromised accounts, identity theft claims, damaged credit, and hours spent undoing access that was never supposed to be granted. Money losses, depending on the method used, are often unrecoverable. Unlike credit card fraud with an issuing bank standing behind the transaction, many scam payments – especially those made through wire transfers, cryptocurrency, or payment apps – leave victims with little institutional recourse.

Why the Numbers Reflect a Structural Problem, Not Just Bad Luck

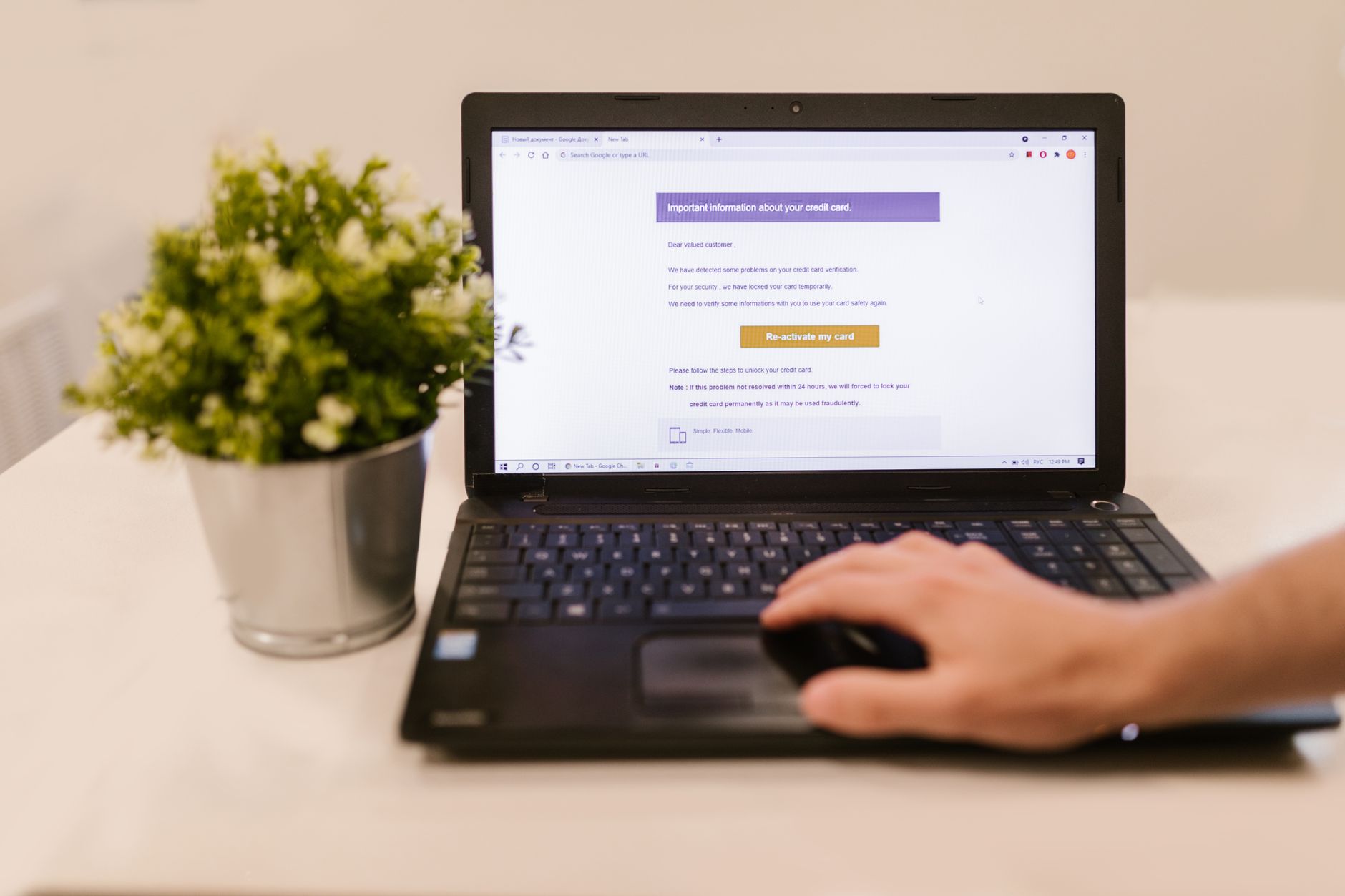

Scam exposure at this scale is not the result of a few particularly gullible people making isolated mistakes. It reflects how thoroughly fraud operations have professionalized over the past decade. Modern scam campaigns are built on large datasets of personal information – phone numbers, email addresses, names, employer information – that allow operators to send targeted, personalized messages at automated scale. A person receiving what looks like a message from their bank, their employer, or a government agency is not being careless by engaging with it. They are responding to something designed with considerable effort to appear legitimate.

The daily bombardment documented in the AP-NORC poll also has a conditioning effect that works in scammers’ favor over time. When people receive dozens of fraudulent contacts per week, they begin to triage rather than scrutinize. Messages get scanned rather than read carefully. Urgency cues – a hallmark of effective scam design – become harder to register as warnings when the baseline level of communication noise is already this high. Fatigue, more than ignorance, has become one of the primary vulnerabilities that fraud operations exploit.

Social media platforms have expanded the attack surface considerably. Unlike phone numbers and email addresses, which can be changed at some cost, social media profiles carry personal details, relationship networks, and behavioral history that make social engineering more effective. A scammer who knows a target’s hometown, employer, family connections, and recent purchases can construct a fraudulent message with enough specificity to sidestep the skepticism that more generic attempts would trigger. The platforms’ role in this environment is a live debate, with users, lawmakers, and companies themselves disagreeing sharply on where responsibility sits.

What Losing Information Actually Costs

The AP-NORC poll groups money and personal information losses together, and while that framing makes statistical sense, the two categories carry different long-term profiles. Money lost to a scam is a discrete event with a calculable dollar figure. Personal information – a Social Security number, a password, account credentials, a date of birth – is a different kind of loss. It does not have an obvious price tag, and the damage from it rarely arrives immediately. Information stolen today can sit in a database for months or years before being deployed against the person it belongs to, which makes connecting the original exposure to a later fraud event genuinely difficult.

For the roughly 3 in 10 Americans who have already experienced a loss, the practical aftermath involves a mix of direct remediation and ongoing vigilance. Freezing credit files, changing passwords across multiple accounts, monitoring financial statements, and disputing fraudulent activity all take time that the victim did not choose to spend. That burden rarely appears in discussions of fraud statistics, which tend to focus on dollar losses and overlook the labor cost of recovery imposed on people who had nothing to gain from the interaction that harmed them.

Law enforcement responses to scam operations face structural limitations that the volume of fraud has made increasingly visible. Many scam operations run across multiple countries, using infrastructure that is difficult to trace and operators who are hard to extradite. Domestic enforcement actions do occur, but the scale of daily contact documented in polls like AP-NORC’s makes clear that takedowns and prosecutions are not keeping pace with the rate at which new campaigns launch. The gap between the number of fraud attempts reaching Americans each day and the number of operators facing legal consequences for those attempts remains very wide.

A Problem With No Clean Edges

What the AP-NORC poll captures is a baseline – a snapshot of where American exposure to scams stands right now, with most people fielding daily attempts and roughly 3 in 10 having already suffered a concrete loss. That baseline has been built over years of expanding digital connectivity, increasingly sophisticated fraud operations, and an information ecosystem in which personal data moves freely enough to supply the raw material for almost any kind of targeted deception. Addressing it will require responses from platforms, financial institutions, telecommunications companies, and law enforcement simultaneously, because no single intervention point controls enough of the pipeline to matter on its own.

The 3 in 10 figure in the AP-NORC data represents people who said they personally lost money or personal information – meaning it almost certainly undercounts the full toll, since many victims do not realize they have been compromised until long after the fact, and others may not connect a financial event they experienced to a scam at all.