The semiconductor rivalry between Nvidia and AMD has reached a new inflection point, with quarterly earnings data exposing a dramatic disparity in both revenue scale and profitability that favors the AI chip leader.

Financial Performance Gap Expands

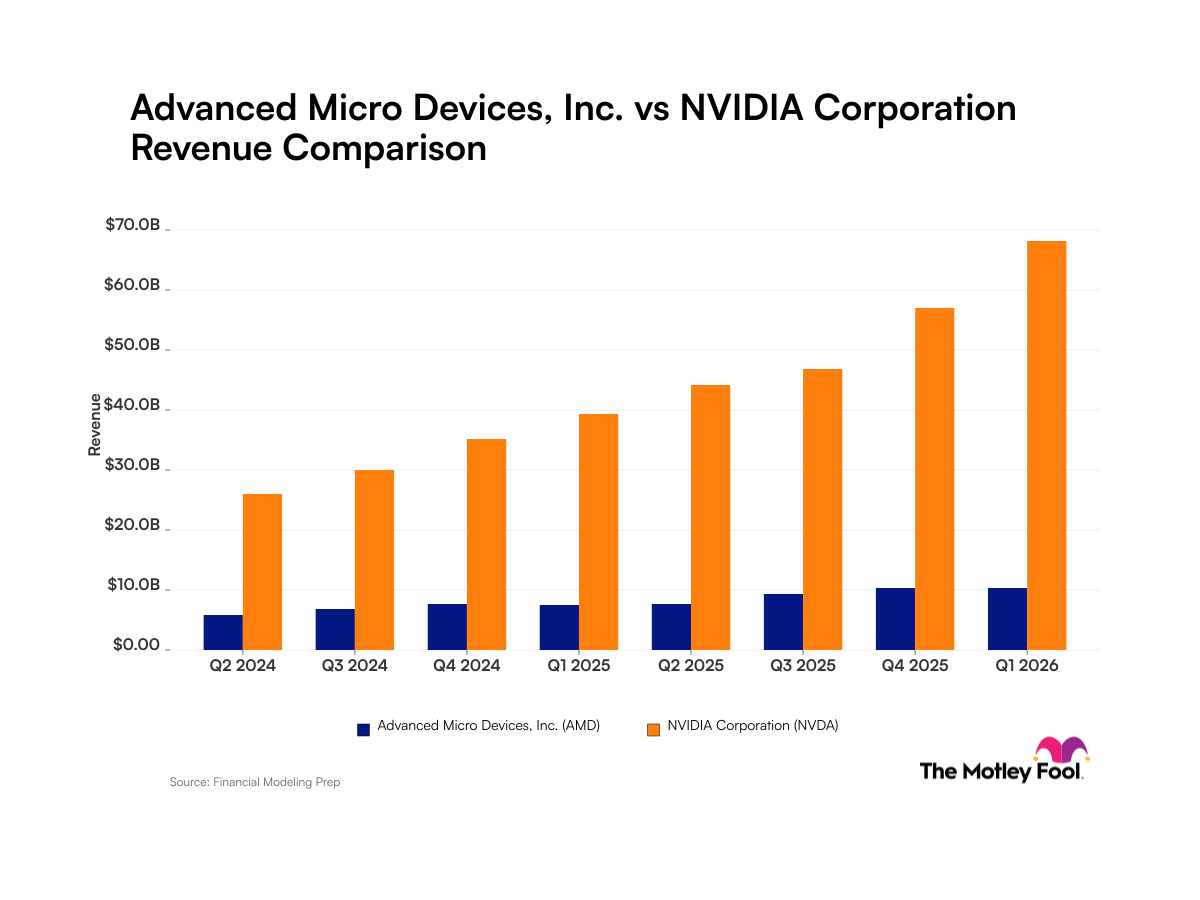

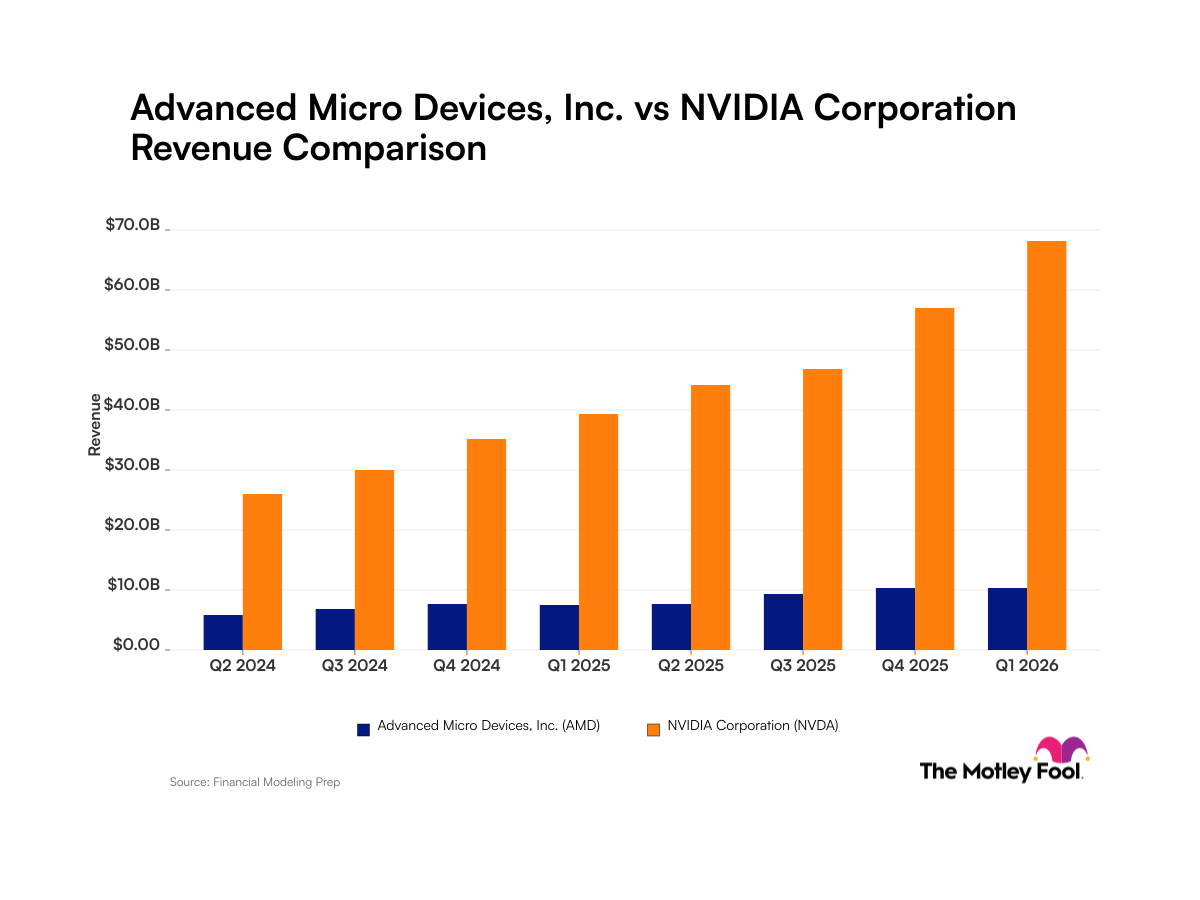

Nvidia’s latest quarterly filings demonstrate revenue figures that dwarf AMD’s comparable numbers, creating a chasm that reflects the different trajectories these chip giants are following. The data center boom has propelled Nvidia’s top-line growth to levels that AMD struggles to match, even as both companies compete for market share in high-performance computing segments.

Profit margins tell an even starker story. Nvidia’s ability to command premium pricing for its AI-focused processors has translated into margin expansion that significantly outpaces AMD’s financial performance. This pricing power stems from Nvidia’s dominant position in artificial intelligence and machine learning applications, where demand continues to outstrip supply.

AMD faces the challenge of competing against a company that has essentially redefined the economics of semiconductor manufacturing. While AMD has made substantial gains in CPU markets and maintains competitive positioning in graphics processing, the revenue scale differential highlights how Nvidia’s strategic focus on AI infrastructure has paid dividends.

The financial metrics reveal more than just current performance-they indicate the compounding advantages that market leadership in high-growth sectors can create. Nvidia’s revenue base provides resources for research and development that AMD must stretch further to match, creating potential long-term competitive implications.

Product Launch Dynamics in Early 2026

Both companies entered 2026 with significant product announcements, yet the market reception and financial impact appear markedly different. These launches represent critical junctures for each company’s strategic positioning, particularly as the AI boom continues to reshape semiconductor demand patterns.

Nvidia’s early 2026 product introductions build upon an already dominant market position, allowing the company to maintain premium pricing while expanding addressable markets. The timing of these launches coincides with enterprise AI adoption cycles, positioning Nvidia to capture increasing wallet share from customers already committed to its ecosystem.

AMD’s product releases during the same period face the harder task of disrupting established customer relationships and proving superior value propositions. The company must demonstrate not just competitive performance but compelling reasons for customers to switch platforms, a challenge made more difficult by Nvidia’s ecosystem advantages and software integration.

The revenue implications of these competing product strategies are becoming apparent in quarterly results. Intel Earnings Lift Tech Giants to Record Market Heights shows how semiconductor earnings have become key indicators for broader tech sector performance, making AMD and Nvidia’s financial divergence particularly noteworthy for investors.

Market analysts are watching whether AMD’s product launches can translate into meaningful revenue acceleration that begins closing the gap with Nvidia. The early 2026 timeframe is viewed as potentially defining for AMD’s ability to compete in the most lucrative semiconductor segments, where Nvidia currently enjoys substantial advantages.

Investment Implications

The revenue and margin disparities between these companies create different investment profiles that appeal to distinct investor preferences. Nvidia’s financial performance suggests a company capitalizing on a dominant market position, while AMD represents a potential turnaround story with higher risk and potentially higher reward characteristics.

Investors must weigh whether AMD’s lower valuation relative to its revenue base compensates for the execution risks inherent in challenging an entrenched market leader. The question remains whether AMD’s 2026 product launches can generate the kind of revenue acceleration needed to narrow the competitive gap, or if Nvidia’s advantages will continue compounding.