AGNC Investment Corporation trades with a dividend yield exceeding 13%, drawing attention from income-focused investors searching for substantial monthly payouts. The mortgage real estate investment trust operates by purchasing agency mortgage-backed securities, using borrowed funds to amplify returns while distributing most profits to shareholders.

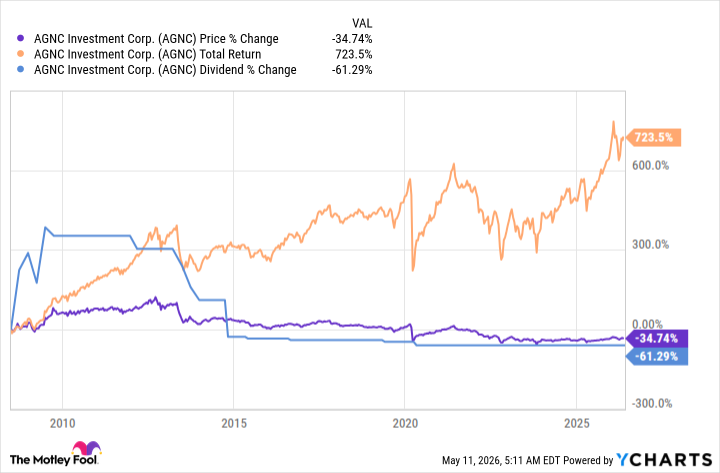

Yet this eye-catching yield comes with a track record that demands scrutiny. AGNC’s dividend history reveals a pattern of cuts that has steadily reduced payments to shareholders over the past decade, raising questions about the sustainability of current distributions.

The mREIT Business Model Creates Yield Volatility

AGNC operates as a mortgage REIT, borrowing short-term funds to purchase longer-term government-backed mortgage securities. This strategy generates profit from the spread between borrowing costs and investment returns, but exposes the company to interest rate fluctuations that can quickly erode margins.

When the Federal Reserve adjusts interest rates, AGNC faces immediate pressure on both sides of its balance sheet. Rising short-term rates increase borrowing costs faster than the company can adjust its mortgage security portfolio, compressing the net interest margin that funds dividend payments. The mREIT sector’s inherent sensitivity to rate changes makes dividend sustainability particularly challenging during periods of monetary policy shifts.

AGNC’s current 13% yield reflects this risk premium. The market prices mortgage REITs based on their vulnerability to interest rate movements, book value fluctuations, and the likelihood of dividend reductions. High yields often signal investor skepticism about payment continuity rather than generous returns.

Dividend Track Record Shows Steady Decline

The company’s dividend history illustrates the challenges facing mortgage REITs in volatile rate environments. AGNC has reduced its monthly distribution multiple times over the past several years, with each cut reflecting pressure from changing market conditions and compressed margins.

These reductions follow a familiar pattern in the mREIT sector, where companies initially maintain high payouts during favorable conditions, then adjust distributions downward when interest rate spreads narrow or book values decline. AGNC’s management has consistently emphasized the need to balance dividend payments with capital preservation, leading to periodic reassessments of distribution levels.

Book Value Erosion Threatens Future Payments

Beyond dividend cuts, AGNC has experienced significant book value deterioration, another warning sign for income investors. Book value per share represents the company’s net worth divided by outstanding shares, and declining book values typically precede dividend reductions in mortgage REITs.

The relationship between book value and dividend sustainability stems from regulatory requirements and practical business constraints. REITs must distribute at least 90% of taxable income to shareholders, but they also need sufficient capital to maintain operations and meet debt obligations. When book values fall substantially, companies often reduce dividends to preserve remaining capital.

AGNC’s book value has declined from previous highs, reflecting unrealized losses on its mortgage security portfolio as interest rates shifted. These paper losses become real constraints on the company’s ability to maintain high dividend payments, particularly if the company needs to sell securities to meet liquidity requirements.

The current dividend yield calculation uses AGNC’s recent share price and annualized distribution rate, but this snapshot doesn’t account for the trajectory of either metric. Share prices for mortgage REITs often decline ahead of dividend cuts, while management teams typically maintain distributions until forced to reduce them by financial constraints.

Income investors considering AGNC face a fundamental question about risk tolerance versus yield requirements. The 13% dividend yield offers substantial monthly income, but the probability of future cuts based on historical patterns and current market conditions suggests this income stream may not prove reliable over time.

Alternative high-yield investments, including high-yield savings accounts, offer more predictable returns without the volatility and dividend risk inherent in mortgage REITs. For investors requiring higher yields than traditional savings products, the trade-off involves accepting either lower current yields with greater stability or higher current yields with significant downside risk.