While investors chase semiconductor stocks riding the artificial intelligence wave, a different technology quietly enables the massive data flows that make AI systems functional. Optical components – the hardware that converts electrical signals to light for high-speed data transmission – represent the unseen foundation supporting AI’s computational demands.

Lumentum Holdings operates at the center of this infrastructure buildout. The company manufactures optical transceivers, lasers, and photonic integrated circuits that handle data traffic between servers, data centers, and cloud networks. As AI workloads explode across hyperscale facilities, these optical connections become the bottleneck that determines system performance.

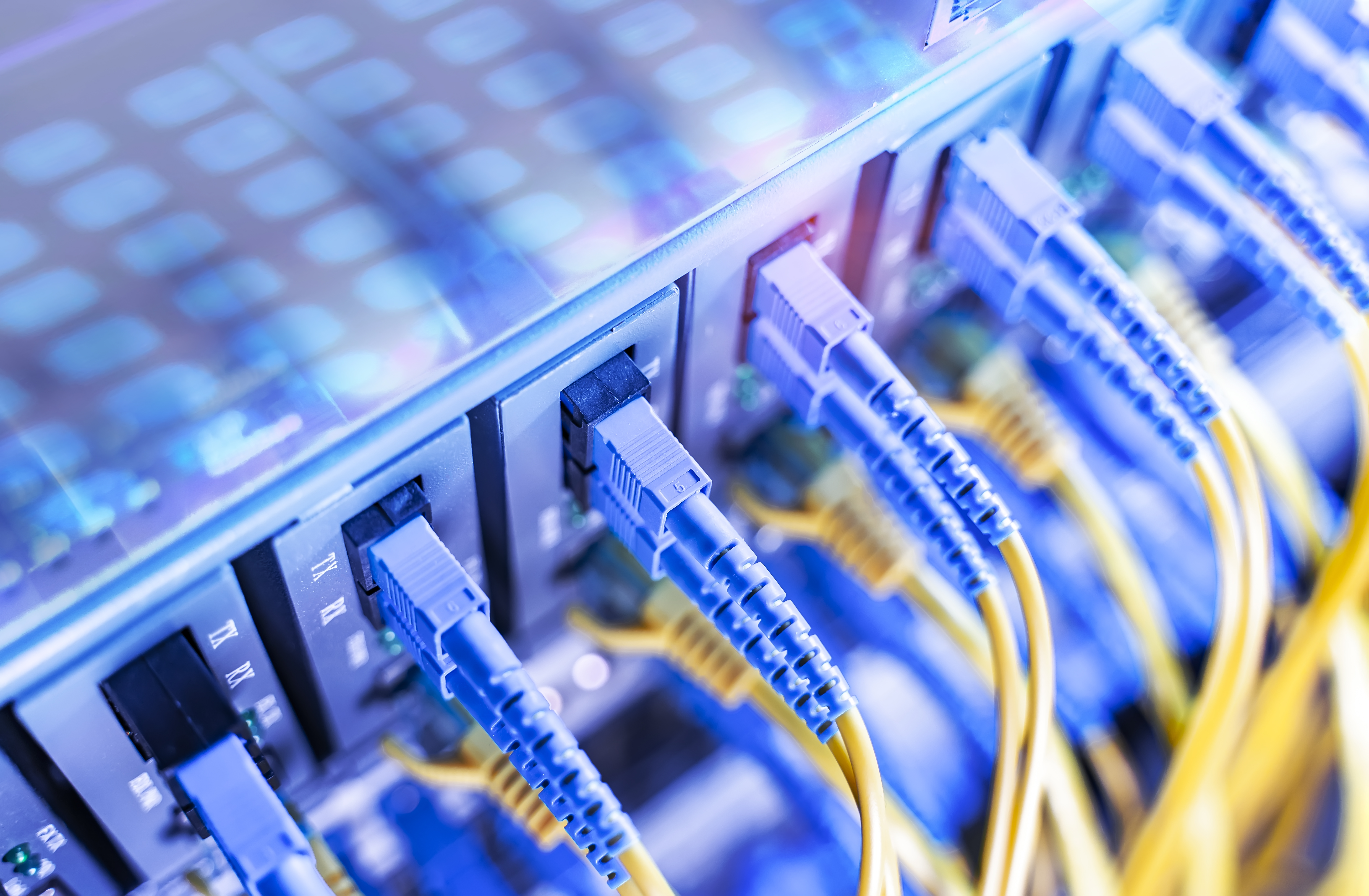

Data Center Demands Drive Optical Innovation

AI training and inference require massive parallel processing across thousands of chips simultaneously. This creates unprecedented demands for high-bandwidth, low-latency connections between processing units, memory systems, and storage arrays. Traditional copper wiring cannot handle these data rates over the distances required in modern data centers.

Optical interconnects solve this problem by using light to carry data at speeds approaching 800 gigabits per second, with roadmaps extending to 1.6 terabits per second and beyond. Lumentum’s transceivers already support 400G and 800G speeds, positioning the company for the transition to even faster standards. Major cloud providers including Microsoft, Amazon Web Services, and Google depend on these components to scale their AI infrastructure.

The shift from 100G to 400G optical connections accelerated dramatically over the past two years. Industry data shows 400G port shipments growing at triple-digit rates as hyperscale operators rebuild their networks for AI workloads. Lumentum captured significant market share during this transition through early investments in silicon photonics technology.

Market Position and Competition

Lumentum competes directly with Broadcom, Marvell Technology, and smaller players like Applied Optoelectronics in the optical transceiver market. The company differentiated itself by developing vertically integrated manufacturing capabilities, controlling everything from laser diodes to final assembly. This integration provides cost advantages and faster time-to-market for new products.

Revenue concentration remains a concern. Lumentum derives roughly 60% of its datacom revenue from its top three customers, creating vulnerability to individual contract losses or pricing pressure. However, this concentration also reflects the company’s strong relationships with the largest cloud providers driving AI adoption.

Financial Performance and Outlook

Lumentum reported datacom revenue of $374 million in its most recent quarter, representing 58% growth year-over-year. Gross margins in the datacom segment reached 32%, up from 28% in the prior year as higher-speed products commanded premium pricing. The company expects this trend to continue as 800G transceivers become the standard for AI cluster interconnects.

Operating leverage becomes apparent as volumes scale. Lumentum’s fixed costs spread across higher unit sales, with each incremental transceiver contributing more to profitability. Management projects datacom gross margins could reach 35% as the product mix shifts toward 800G and next-generation speeds.

The company invested $89 million in research and development during the quarter, equivalent to 13% of total revenue. These investments focus on co-packaged optics – a technology that integrates optical transceivers directly with switching chips to reduce power consumption and latency. Early trials with hyperscale customers show promising results for this approach.

Balance sheet strength provides flexibility for continued investment. Lumentum maintains $847 million in cash and short-term investments against $435 million in total debt. This financial cushion allows the company to fund capacity expansions and technology development without relying on external financing.

Risks and Valuation Considerations

Cyclical demand patterns create volatility in optical component sales. Data center operators typically purchase equipment in large batches to support major infrastructure projects, leading to lumpy quarterly results. Lumentum experienced this firsthand when cloud spending slowed in 2022, causing revenue to decline 23% year-over-year.

Technology transitions also introduce execution risk. The shift to 800G and beyond requires significant engineering investments with uncertain payoffs. If Lumentum fails to deliver competitive products on schedule, customers may switch to alternative suppliers. The optical networking market offers little forgiveness for missed product cycles.

Current valuation reflects optimistic growth expectations. Lumentum trades at 28 times forward earnings despite operating in a historically cyclical industry. This multiple assumes continued strong demand for high-speed optical interconnects and successful execution of next-generation product introductions.

Supply chain constraints could limit Lumentum’s ability to capitalize on growing demand. The company relies on specialized semiconductor foundries for key components, creating potential bottlenecks during periods of strong market growth. Recent shortages of optical components have already extended customer lead times and pressured pricing in some market segments.